For traders exploring different position sizing methodologies, the Anti-Martingale Strategy represents a compelling alternative to more risk-intensive approaches. Unlike its counterpart, the Martingale Strategy, this method focuses on capital preservation while still allowing for substantial profit potential during favorable market conditions. Whether you're new to trading or looking to refine your risk management techniques, understanding this positive progression system can provide valuable insights into how professional traders approach position sizing.

Who Developed the Anti-Martingale Strategy?

The Anti-Martingale Strategy evolved as a direct response to the high-risk Martingale approach. While no single individual is credited with its creation, the strategy emerged from professional trading and gambling circles as practitioners sought safer alternatives to negative progression systems.

The concept gained substantial recognition through the work of Larry Williams, a renowned trader and author who incorporated similar principles in his "percent risk" money management system during the 1970s and 1980s. Williams emphasized increasing position size during winning streaks while maintaining strict risk control parameters.

Further development and popularization of the approach came through the influential works of trading psychologist Dr. Van K. Tharp, who extensively explored position sizing methodologies in his books on risk management. Notable traders like Ed Seykota and Paul Tudor Jones have also advocated for variations of positive progression systems in their trading approaches.

While these figures contributed substantially to the strategy's development and popularization, the Anti-Martingale approach is best understood as an evolutionary development within professional trading communities rather than the creation of any single theorist.

What is the Anti-Martingale Strategy?

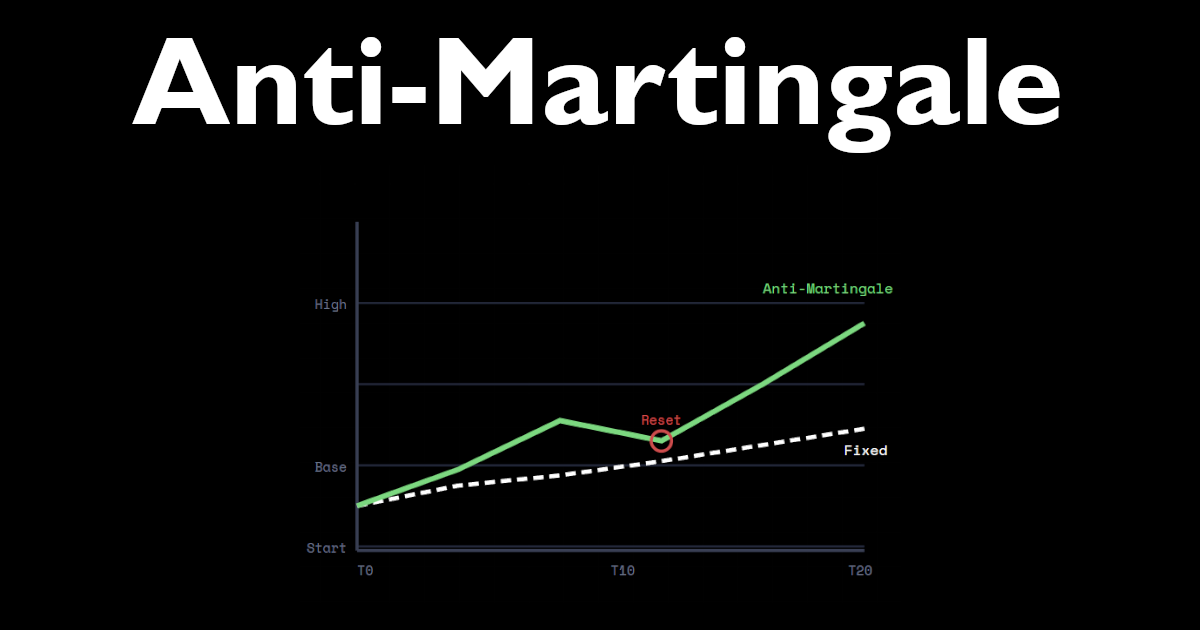

The Anti-Martingale Strategy is a positive progression system for position sizing that increases exposure during winning streaks and reduces it during losing periods. This approach directly inverts the principles of the traditional Martingale system.

Basic Mechanics:

- Start with an initial position size based on a predetermined percentage of your trading capital (typically 1-2%)

- After a winning trade, increase your position size for the next trade (often by 50-100% of the previous size)

- After a losing trade, decrease your position size (typically returning to your initial position size)

- Continue increasing position size during winning streaks, potentially until reaching a predetermined maximum

- Maintain strict position sizing limits to prevent overexposure

For example, if your initial position is $1,000 and you win, your next position might be $1,500 or $2,000. If that trade also wins, you might increase to $2,250 or $3,000. However, upon experiencing a loss at any point, you would return to your initial $1,000 position size.

Mathematical Basis:

The Anti-Martingale approach aligns with several mathematical concepts in trading:

- Positive Expected Value: By increasing exposure during periods when your strategy is performing well (suggesting favorable market conditions), you maximize returns when your edge is strongest.

- Geometric Growth: Compounding returns through progressive position sizing creates potential for geometric rather than arithmetic portfolio growth.

- Limited Drawdown: By reducing exposure after losses, the strategy naturally limits drawdowns during unfavorable periods.

Let's examine a sequence:

- First trade: $1,000 position (Win of 10%) → Profit: $100, New Balance: $10,100

- Second trade: $2,000 position (Win of 10%) → Profit: $200, New Balance: $10,300

- Third trade: $4,000 position (Loss of 5%) → Loss: $200, New Balance: $10,100

- Fourth trade: Return to $1,000 position

This approach can be further refined by using a fixed percentage of current capital rather than fixed dollar amounts, creating a natural scaling mechanism as account size changes.

Required Assumptions for the Anti-Martingale Strategy to Work

For the Anti-Martingale strategy to function effectively, several key assumptions must be accepted:

- Persistence of Market Conditions: The strategy assumes that market conditions that produced recent wins are likely to persist for some period, creating "streaks" of favorable outcomes.

- Positive Expected Value: Your trading system must have a positive expected value (edge) over a large sample of trades. Without this fundamental requirement, no position sizing strategy can produce long-term profits.

- Psychological Discipline: Traders must have the discipline to reduce position sizes after losses rather than attempting to "recover" losses through larger positions.

- Sufficient Capital: You must have enough trading capital to withstand normal drawdown periods while maintaining appropriate position sizes.

- Risk Management Priority: You must prioritize risk management over maximizing any single trading opportunity.

- Logical Exit Criteria: The strategy requires clear exit parameters for both winning and losing trades that are based on market conditions rather than emotional responses.

How to Use the Anti-Martingale Strategy in a Trading Plan

Implementing the Anti-Martingale Strategy requires a systematic approach with clearly defined parameters:

Step 1: Establish Your Base Risk Parameters

Before applying any progressive sizing system, define your fundamental risk guidelines:

- Determine your initial risk per trade (typically 1-2% of total capital)

- Calculate position sizes based on specific stop-loss levels for each trade

- Establish the maximum percentage of your account you'll risk on any single trade (typically 5-10%)

Step 2: Define Your Progression Rules

Create clear rules for how position sizes will increase during winning periods:

- Specify the exact percentage increase after each win (e.g., 50%, 100%)

- Determine whether to use fixed dollar amounts or percentages of current capital

- Set a cap on the maximum number of consecutive increases (e.g., no more than 4 consecutive increases)

Step 3: Establish Reset Conditions

Define precisely when position sizes will be reduced:

- After any single losing trade

- When a predetermined drawdown threshold is reached

- When market conditions change significantly (e.g., volatility increases)

- At scheduled intervals (e.g., weekly or monthly resets)

Step 4: Incorporate Market Filters

Enhance the strategy by adding conditions that must be met before increasing position sizes:

- Technical conditions (e.g., trading in the direction of the prevailing trend)

- Volatility parameters (e.g., only increase positions during normal volatility conditions)

- Correlation with broader market conditions

- Seasonal or time-based factors that affect your specific trading instruments

Step 5: Create Detailed Record-Keeping Systems

Develop tracking systems to monitor the strategy's performance:

- Document each trade with its position size and sequence in the progression

- Track performance metrics during different market conditions

- Compare results between standard fixed-sizing and Anti-Martingale periods

- Note psychological observations during both winning and losing sequences

Step 6: Implement Safety Valves

Add protective mechanisms to prevent excessive risk:

- "Circuit breakers" that automatically reset position sizes after reaching specific profit targets

- Overall exposure limits across all positions

- Rules for taking partial profits as position sizes increase

- Time-based resets that return to the base position size after a defined period

Pitfalls of the Anti-Martingale Strategy

Despite its advantages over the Martingale approach, traders should be aware of several potential challenges:

- False Pattern Recognition: Winning streaks can occur randomly, even with a negative expectancy system. Increasing position sizes based on random sequences can amplify losses when reversion occurs.

- Overconfidence Bias: Consecutive wins often create overconfidence, leading traders to exceed their predetermined position sizing rules or ignore warning signs in market conditions.

- Psychological Resistance: Many traders find it psychologically difficult to increase position sizes after wins, fearing they might "jinx" their streak or be entering at peak prices.

- Inappropriate Application: The strategy works best with certain trading styles and market conditions. Applying it universally across all trading scenarios can lead to suboptimal results.

- Inadequate Testing: Traders often implement the strategy without sufficient backtesting or simulation, leading to unexpected results in live trading.

- Position Size Calibration: Determining the optimal percentage increase after wins requires careful calibration based on the specific characteristics of your trading system.

- Market Transition Lags: Markets can shift from trending to ranging conditions quickly, but recognizing these transitions often comes with a lag, resulting in larger positions during unfavorable conditions.

- Account Size Limitations: Smaller accounts may not have sufficient capital to properly implement a graduated position sizing strategy while maintaining appropriate risk parameters.

Simulator Assignment: Testing the Anti-Martingale Strategy

Objective:

Gain practical experience with the Anti-Martingale Strategy while documenting its performance characteristics under various market conditions. Before you begin, remember to Reset Game History in your Dashboard to ensure you're not including any old data in your test results.

Setup:

- The Trading Blitz simulator provides a virtual account of $100,000

- Set your initial position risk at 1% of capital ($1,000 risk per trade)

- Establish clear entry and exit criteria based on your preferred trading strategy

- Create a tracking spreadsheet with these columns:

- Trade number

- Current account balance

- Position size

- Percentage of account risked

- Entry price and date

- Exit price and date

- Profit/Loss

- Running equity curve

- Position in sequence (initial, 1st increase, 2nd increase, etc.)

- Market condition notes

Practice Exercises:

Exercise 1: Basic Implementation

- Trade liquid stocks using your established strategy

- After each win, increase your next position size by 50%

- After each loss, return to your initial 1% risk position size

- Complete 20 trades using this approach

- Calculate performance metrics and compare to what would have happened with fixed position sizing

Exercise 2: Varied Increase Percentages

- Conduct three separate testing periods with different increase percentages:

- Conservative: 30% increase after wins

- Moderate: 50% increase after wins

- Aggressive: 100% increase after wins

- Complete 15 trades with each parameter set

- Compare risk-adjusted returns and maximum drawdowns across the three approaches

Exercise 3: Market Condition Filters

- Add filters that must be satisfied before increasing position size:

- Only increase position size when trading in the direction of the 20-day moving average

- Only increase when volatility (ATR) is below its 10-day average

- Reset to base size when these conditions are no longer met

- Compare performance with and without these filters

- Document how these filters affect the frequency of position size increases

Performance Tracking:

Track these key statistics during your simulations:

- Win rate with base position size vs. increased position sizes

- Average profit per trade at different position size levels

- Maximum consecutive winners and losers

- Total return compared to fixed position sizing

- Maximum drawdown as a percentage of account

- Sharpe ratio and other risk-adjusted return metrics

- Emotional comfort level at different position sizes (subjective rating 1-10)

Review Process:

After completing your simulator exercises:

- Analyze which progression parameter produced the best risk-adjusted returns

- Identify which market conditions were most favorable for the strategy

- Determine how the strategy affected your trading psychology

- Calculate the optimal reset conditions based on your results

- Develop a customized Anti-Martingale framework suited to your specific trading approach

Conclusion

The Anti-Martingale Strategy represents a more sustainable approach to position sizing than its high-risk counterpart, the Martingale Strategy. By increasing exposure during favorable periods and reducing risk during drawdowns, this method aligns with professional risk management principles while still providing mechanisms for capital growth.

The key to successfully implementing this strategy is maintaining strict discipline regarding position increases and decreases. Many traders find it easier psychologically to increase position sizes after wins than to return to base size after losses, yet adhering to both aspects is equally important for long-term success.

When properly implemented with appropriate filters and safeguards, the Anti-Martingale approach can enhance returns from a profitable trading system while helping to protect capital during inevitable losing periods. The Trading Blitz simulator provides an ideal environment to test various parameters and gain comfort with the strategy before applying it to real-world trading.

Remember that no position sizing strategy can turn a negative expectancy system into a profitable one. The Anti-Martingale approach should only be applied to trading methods that have demonstrated a positive edge through rigorous testing and evaluation. When combined with sound technical or fundamental analysis, this approach can become a valuable component of your overall trading methodology.

As with all aspects of trading, personalization is essential. Through careful testing and documentation using the Trading Blitz simulator, you'll be able to determine the specific Anti-Martingale parameters that best complement your trading style, risk tolerance, and financial objectives.

Free Cash-Prize Touraments

We run free cash-prize tournaments (no entry fee required) when we go live on YouTube. Be sure to subscribe to our channel - @TradingBlitzSimulator - to get alerted when we go live next.

Disclaimer: Trading involves substantial risk of loss and is not appropriate for all investors. The information provided on Trading Blitz is for educational and informational purposes only. Nothing on this platform, including this article, constitutes financial advice, investment advice, or a recommendation to buy or sell any security. Simulated trading results do not guarantee or predict future performance in live markets. Past performance, whether real or simulated, is not indicative of future results. Always consult a qualified financial professional before making any investment decisions. For additional information, please see our Terms of Service.

Affiliate Disclosure: Some links in this article may be affiliate links. If you click through and make a purchase, Trading Blitz may earn a small commission at no additional cost to you. We only reference tools and resources we believe are relevant to traders.